Lesson 7. Respecting Markets

Incorporating a macro framework into your investing framework can be quite valuable. It helps to avoid the situation where it is difficult to see “the forest through the trees”.

It is true that equity markets tend to go higher over time. That said, they can go through periods of significant correction and multiple contraction. It is during these periods that an understanding of macro can be most valuable. Multiples tend to trough during periods of weak growth/recession.

One multiple from Lesson 5 that is especially important is the earnings multiplier (P/E ratio) - a financial metric that has been used for many years to determine the value of a company. It is calculated by dividing the market price per share by the earnings per share of a company. The earnings multiplier is an important tool for investors because it allows them to compare the value of different companies in the same industry.

The 1920s

The earnings multiplier was not widely used as a metric for valuing companies. Instead, investors relied on other metrics such as dividend yield and price-to-book ratio. That said, during the 1920s, the average earnings multiplier for companies in the Dow Jones Industrial Average (the Dow) was around 15.

The 1930s

This was a difficult time for the stock market and the economy as a whole coming out of the Great Depression. The earnings multiplier for companies in the Dow fell to an average of around 8.

The 1940s

This period saw a return to growth for the economy and the stock market. The earnings multiplier for companies in the Dow rose to an average of around 10. This was due to the fact that many companies were reporting higher earnings as the economy improved.

The 1950s and 1960s

The post WW II period was one of sustained growth for the economy and the stock market. The earnings multiplier for companies in the Dow rose to an average of around 20. This was due to the fact that investors were willing to pay more for companies that were growing and had strong earnings.

The 1970s

This was a difficult time for the economy and the stock market. The earnings multiplier for companies in the Dow fell to an average of around 8. This was due to the combination of high inflation and a stagnant economy. High inflation tends to result in multiple compression, while more stable/low inflation environments result in expansion.

The 1980s and 1990s

This was a period of sustained growth for the economy and the stock market. The earnings multiplier for companies in the Dow rose to an average of around 25.

The 2000s

This was a difficult time for the stock market due to the dot-com bubble and the Great Financial Crisis in 2008. The earnings multiplier for companies in the Dow fell to an average of around 15. This was due to the fact that investors were more cautious and were not willing to pay as much for companies that were not performing well.

The 2010s

This was a period of sustained growth for the stock market. The earnings multiplier for companies in the Dow rose to an average of around 20. This was also driven by the backstops provided to very easy financial conditions and the era of Quantitative Easing (QE) and fiscal backstops.

It is important to remember that current (as of April 2026) multiples are near historic highs.

Remember, multiples don’t “rise just because growth is good”. In my opinion, they rise because money is cheap, inflation is contained, and investors trust the system.

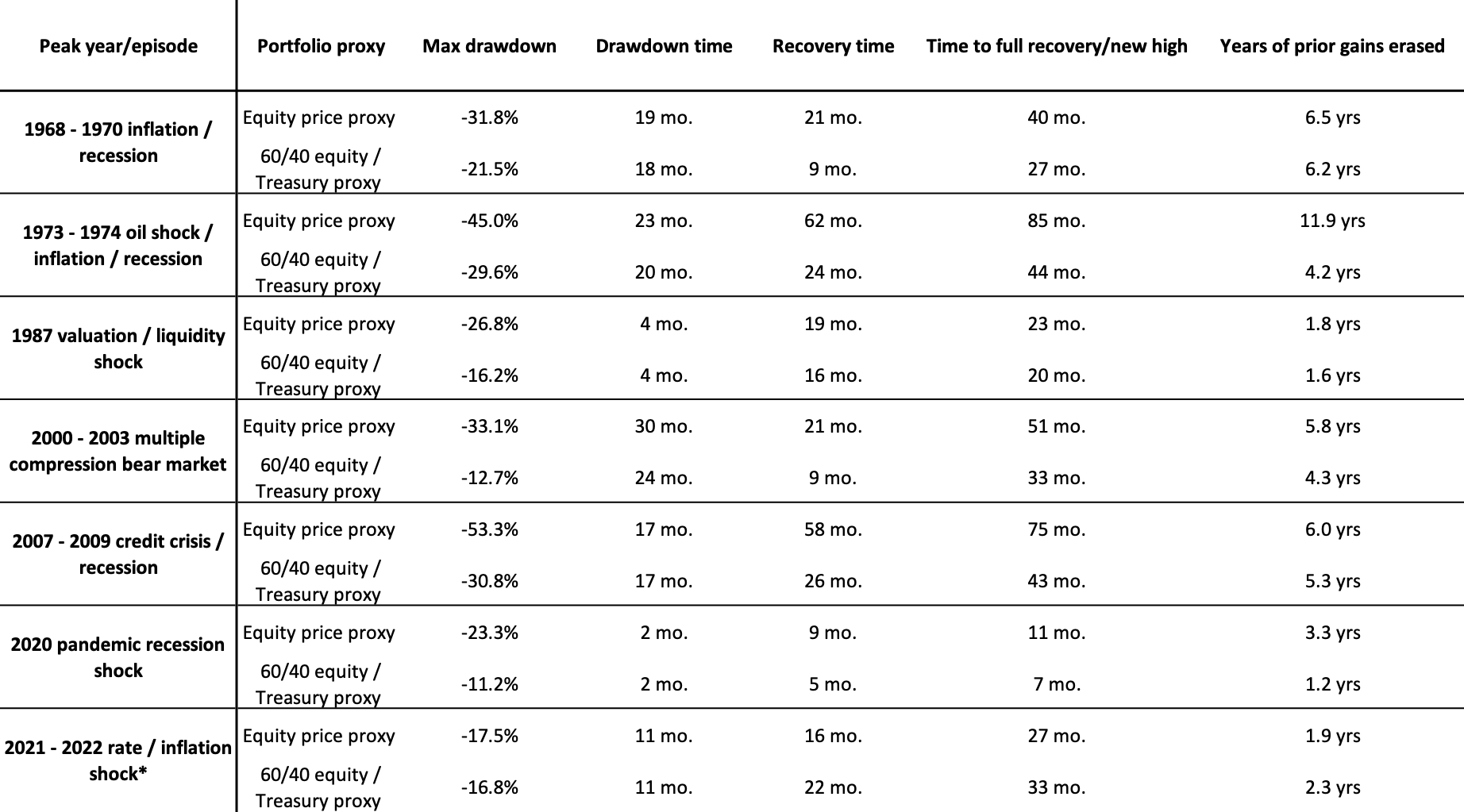

This exhibit below uses simplified public-data proxies to illustrate the relative depth and recovery profile of major drawdowns. The figures are calculated from an equity price proxy and a simplified Treasury proxy and are intended as directional comparisons rather than exact historical portfolio results.

*Commonly treated as a bear market, though in this simplified monthly proxy the decline falls short of the formal -20% threshold.

Source: Calculations using Organization for Economic Co-operation and Development, Financial Market: Share Prices for United States [SPASTT01USM661N], and Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis [GS10], retrieved from FRED, Federal Reserve Bank of St. Louis.

Key Takeaways

Macro is often most valuable during periods of correction, multiple contraction, and broader market stress.

The P/E ratio is one of the key multiples in equity investing because it shows how much investors are willing to pay for each dollar of earnings.

Earnings multiples have generally been lower during recessions, inflationary periods, and tighter financial conditions, and higher during more stable, lower-inflation environments.

Multiples do not expand simply because growth is strong; rates, liquidity, inflation, and confidence in the broader system also shape valuation.

Starting valuation matters because higher multiples can leave markets more exposed to drawdowns and slower recoveries.

Major drawdowns can erase years of gains, while more balanced portfolios have often experienced shallower declines and faster recoveries than more concentrated exposure.

This website and its content are provided for informational and educational purposes only and do not constitute investment, financial, legal, tax, or other professional advice, nor any offer, recommendation, solicitation, or invitation to buy or sell any security or financial instrument. Any views expressed are solely the author’s own as of the date of publication, are subject to change without notice, and do not necessarily reflect the views, positioning, or risk of Schonfeld.